Loan Default in India – What Happens and How to Handle It Legally | DM Legal Services

Loan Default in India: What Happens and How to Handle It Legally

Loan default in India is a growing concern as borrowers face financial stress due to job loss, medical emergencies, or business slowdowns.

Whether it’s a secured loan, an unsecured personal loan, or a credit card default, understanding your legal rights and the proper steps to manage the situation can help you protect your finances and reputation.

In this article, DM Legal Services explains what happens when a loan default occurs in India, the difference between secured and unsecured defaults, and how to handle them effectively.

🔹 Understanding Loan Default in India

A loan default happens when a borrower fails to make EMI payments as agreed with the lender. In India, financial institutions have specific legal remedies to recover their dues, depending on the type of loan.

Broadly, loans are classified as:

- Secured Loans — backed by collateral such as property, gold, or a vehicle.

- Unsecured Loans — not backed by any collateral, such as credit cards or personal loans.

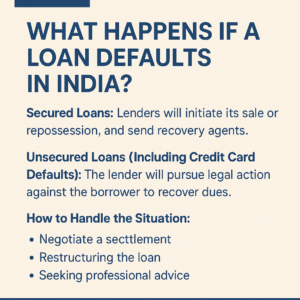

🔹 Secured Loan Default in India: Legal Consequences and Process

When you default on a secured loan, the lender’s primary recourse is against the collateral. Under the SARFAESI Act, 2002, lenders can initiate recovery actions after issuing a 60-day notice.

- Notice of Default:

The bank sends a formal demand notice to repay dues within a specific period. - Repossessing the Asset:

If payment isn’t made, the lender can take possession of the pledged property or vehicle. - Auction and Sale:

After repossession, the asset can be auctioned to recover outstanding amounts. - Legal Recourse:

If the asset value doesn’t cover the full debt, lenders may file a case before the Debt Recovery Tribunal (DRT) for the balance. - Credit Score Damage:

A secured loan default in India severely affects your CIBIL score, making future borrowing difficult.

🔹 Unsecured Loan Default and Credit Card Default in India

An unsecured loan default occurs when a borrower fails to repay a loan without collateral — such as a personal or credit card loan.

Here’s what typically happens:

- Collection Efforts Begin:

Lenders and collection agencies contact the borrower through calls and notices. - Legal Notice or Civil Suit:

If dues remain unpaid, lenders can file a civil suit for recovery under the Indian Contract Act or take action under the Negotiable Instruments Act if cheques were involved. - Credit Report Impact:

Defaults are reported to CIBIL and other credit bureaus, lowering your score and reputation. - Police or Legal Action:

In cases involving fraudulent intent or cheque bounce, police complaints or FIRs may be filed.

🔹 How to Handle a Loan Default in India

If you’re struggling to repay your loan, it’s essential to take proactive and lawful steps to minimize damage:

- Communicate with Your Lender Early:

Inform the lender about financial hardships. Many banks offer loan restructuring, EMI moratoriums, or payment deferrals to genuine cases. - Negotiate a One-Time Settlement (OTS):

If you cannot repay the entire amount, negotiate a one-time settlement to close the loan legally. - Avoid Ignoring Legal Notices:

Respond promptly to all communication from your lender. Non-response can escalate the issue legally. - Seek Professional Legal Help:

Consulting a loan default lawyer in India helps protect your rights, manage negotiations, and handle harassment from recovery agents. - Rebuild Your Financial Health:

After resolving the default, focus on rebuilding your credit by maintaining timely payments and monitoring your CIBIL score.

⚖️ How DM Legal Services Can Help You

At DM Legal Services, we specialize in handling loan default cases in India. Our team assists clients with:

- Negotiating with lenders for settlements or restructuring

- Representing borrowers before DRT and civil courts

- Protecting against unlawful recovery methods

- Drafting and reviewing repayment and settlement agreements

We believe every financial challenge has a legal solution — our goal is to help you resolve loan defaults with professionalism, dignity, and legal clarity.

🧭 Key Takeaway

A loan default in India can harm your credit, lead to asset seizure, and result in legal consequences — but it doesn’t have to ruin your financial life. By communicating with lenders, taking timely legal advice, and acting transparently, you can regain financial stability.

📞 For expert assistance with loan default cases in India, contact DM Legal Services today.

🌐 Visit: www.dmlegalservices.in/loan-default-in-india

📧 Email: info@dmlegalservices.in

Previous Post

Previous Post Next Post

Next Post